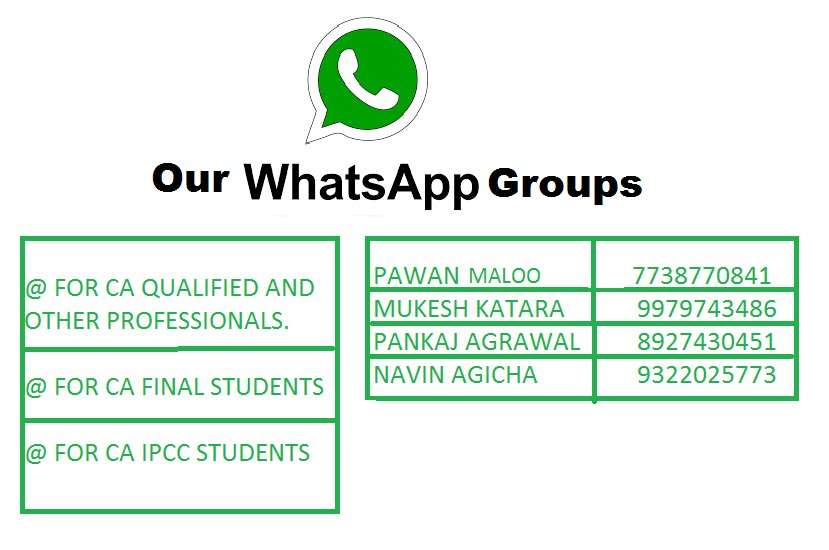

Navin Agicha

Friday 21 August 2015

Monday 10 August 2015

Thursday 6 August 2015

Sunday 2 August 2015

Wednesday 29 July 2015

CA FINAL DT SUMMARY NOTES BY ARUN SONI

TONAGE TAX

CLICK HERE TO DOWNLOAD

TRANSFER PRICING

CLICK HERE TO DOWNLOAD

FINANCE ACT 2014

CLICK HERE TO DOWNLOAD

TAXATION OF VARIOUS ENTITIES

CLICK HERE TO DOWNLOAD

SECTION 10 NOTES

CLICK HERE TO DOWNLOAD

CLICK HERE TO DOWNLOAD

TRANSFER PRICING

CLICK HERE TO DOWNLOAD

FINANCE ACT 2014

CLICK HERE TO DOWNLOAD

TAXATION OF VARIOUS ENTITIES

CLICK HERE TO DOWNLOAD

SECTION 10 NOTES

CLICK HERE TO DOWNLOAD

Tuesday 28 July 2015

CA FINAL NOTES BY ASHWIN GYANCHANDANI

SA Memory Tip

CLICK HERE TO DOWNLOAD

Difference between Audit Procedure & Audit Technique

CLICK HERE TO DOWNLOAD

Significance of SA 500, 315, 330, 450, 240 & 402

CLICK HERE TO DOWNLOAD

Audit Procedure for Obtaining Audit Evidences

CLICK HERE TO DOWNLOAD

How to write answers for Professional Ethics

CLICK HERE TO DOWNLOAD

CLICK HERE TO DOWNLOAD

Difference between Audit Procedure & Audit Technique

CLICK HERE TO DOWNLOAD

Significance of SA 500, 315, 330, 450, 240 & 402

CLICK HERE TO DOWNLOAD

Audit Procedure for Obtaining Audit Evidences

CLICK HERE TO DOWNLOAD

How to write answers for Professional Ethics

CLICK HERE TO DOWNLOAD

CA FINAL IDT NOTES NOV 2015

IDT CASE LAW

CLICK HERE TO DOWNLOAD

FTP NOV 15

CLICK HERE TO DOWNLOAD

IDT BOOK( UPDATED APRIL 2015)

CLICK HERE TO DOWNLOAD

CLICK HERE TO DOWNLOAD

FTP NOV 15

CLICK HERE TO DOWNLOAD

IDT BOOK( UPDATED APRIL 2015)

CLICK HERE TO DOWNLOAD

Friday 17 April 2015

REGARDING NON DEDUCTION AND SHORT DEDUCTION OF TDS AS PER FINANCE ACT 2014 APPLICABLE FOR MAY 2015 CA IPCC AND FINAL

Section 40(a)(ia)

[any interest, commission or brokerage, [rent, royalty,] fees for professional services or fees for technical services payable to a resident, or amounts payable to a contractor or sub-contractor, being resident, for carrying out any work (including supply of labour for carrying out any work)], on which tax is deductible at source under Chapter XVII-B and such tax has not been deducted or, after deduction, [has not been paid on or before the due date specified in sub-section (1) of section 139 :]

[Provided that where in respect of any such sum, tax has been deducted in any subsequent year, or has been deducted during the previous year but paid after the due date specified in sub-section (1) of section 139, [thirty per cent of] such sum shall be allowed as a deduction in computing the income of the previous year in which such tax has been paid :]

[Provided further that where an assessee fails to deduct the whole or any part of the tax in accordance with the provisions of Chapter XVII-B on any such sum but is not deemed to be an assessee in default under the first proviso to sub-section (1) of section 201, then, for the purpose of this sub-clause, it shall be deemed that the assessee has deducted and paid the tax on such sum on the date of furnishing of return of income by the resident payee referred to in the said proviso.]

Disallowance for non-deduction or non-payment of TDS:

Under section 40(a)(ia) of the Act, in case of payments made to resident, the deductor is allowed to claim deduction for payments as expenditure in the previous year of payment, if tax is deducted during the previous year and the same is paid on or before the due date specified for filing of return of income under section 139(1) of the Act.In case of non-deduction or non-payment of tax deducted at source (TDS) from certain payments made to residents, the entire amount of expenditure on which tax was deductible is disallowed under section 40(a)(ia) for the purposes of computing income under the head “Profits and gains of business or profession”. The disallowance of whole of the amount of expenditure results into undue hardship.

In order to reduce the hardship, non-deduction or non-payment of TDS on payments made to residents as specified in section 40(a)(ia) of the Act, the disallowance shall be restricted to 30% of the amount of expenditure on which TDS is not deducted.

Earlier, 100% of such amount is disallowed.

Earlier, the non-deduction or non-payment of TDS on payments made to residents results in disallowance only with respect to certain specified categories of payments (viz. interest, commission, brokerage, rent, royalty, fee for technical services or fee for professional services).

NOW section 40(a)(ia) of the I-T Act to increase the scope of disallowance to every category of payment made to a resident on which tax is required to be deducted at source under Chapter XVII-B of the I-T Act.

Controversy:-

What amount to be disallowed us 40(a)(ia) on non deduction or short deduction?

Views:-

1) 30% of whole amount.

2) 30% of amount which TDS not deducted or short deducted (Proportional basis).

3) disallowance under section 40(a)(ia) is only for non deduction of tax at source and not short-deduction of tax.

Analysis of views

1) First view is illogical as if person have deducted and paid tax on maximum amount but he didn’t deducted and paid on minor amount.

2) Second view is True and fair view as 30% disallowance to be made on proportionally .

3) Third view is illogical because section 40(a)(ia) says that fails to deduct the whole or any part of the tax.

Let us understand it with some Examples:-

1) Tax to be deducted us 194J @10% is Rs 10,000/- on Rs 1,00,000/- and no deducted and paid. What will be amount of disallowance?

Answer:- No tax deducted and paid on Rs 1,00,000.

So Amount of disallowance will be Rs 30,000/- (30% of Rs 1,00,000/-) and if it is paid after due date then Rs 30,000/- will be allowed as deduction in next year.

2) Tax to be deducted us 194J @10% is Rs 10,000/- on Rs 1,00,000/- and actually deducted and paid Rs 1,000/-. What will be amount of disallowance?

Answer:- Tax deducted and paid is Rs 1,000/- means on Rs 10,000/- tax is deducted and on Rs 90,000/- tax is not deducted.

So Amount of disallowance will be Rs 27,000/- (30% of Rs 90,000/-) and if it is paid after due date then Rs 27,000/- will be allowed as deduction in next year.

This is solved based on second view discussed above and if we take first view then disallowance will be Rs 30,000 which will be incorrect. To prove that first view is incorrect , let discuss example no 3.

3) Tax to be deducted us 194J @10% is Rs 10,000/- on Rs 1,00,000/- and actually deducted and paid Rs 9,000/-. What will be amount of disallowance?

Answer:- Tax deducted and paid is Rs 9,000/- means on Rs 90,000/- tax is deducted and on Rs 10,000/- tax is not deducted.

So Amount of disallowance will be Rs 3,000/- (30% of Rs 10,000/-) and if it is paid after due date then Rs 3,000/- will be allowed as deduction in next year.

This is solved based on second view discussed above and if we take first view then disallowance will be Rs 30,000 which will be incorrect. Hence with this example it is proved that first view is incorrect.

Final Conclusion is that in case of non deduction and short deduction amount disallowed us 40(a)(ia) will be 30% of amount which TDS not deducted or short deducted (Proportional basis).

Thanks and Regards,

Navin Agicha

agicha.navin@gmail.com

Thursday 16 April 2015

Wednesday 15 April 2015

CA FINAL MAY 2015 GOOD NOTES INCLUDING MOCK TEST AND IDT CHARTS

Income Tax Fact Track Quick Revision for May 2015 and November 2015

CLICK HERE TO DOWNLOAD

IDT AMENDMENTS BY PADHUKA

IDT CASE LAW SUMMARY

DT CASE LAW SUMMARY

CA FINAL MAY 15 RTP

WEALTH TAX SUMMARY

CA FNAL MOCK TEST MAY 2015

QUESTIONS

SOLUTIONS

CA FINAL IDT CHARTS MAY 2015

CA FINAL AUDIT AMENDMENTS MAY 2015

Sunday 12 April 2015

CA FINAL MAY 2015

Income Tax Fact Track Quick Revision for May 2015 and November 2015

CLICK HERE TO DOWNLOAD

IDT AMENDMENTS BY PADHUKA

IDT CASE LAW SUMMARY

DT CASE LAW SUMMARY

CA FINAL MAY 15 RTP

WEALTH TAX SUMMARY

CA FNAL MOCK TEST MAY 2015

QUESTIONS

SOLUTIONS

CA FINAL IDT CHARTS MAY 2015

CA FINAL AUDIT AMENDMENTS MAY 2015

Saturday 24 January 2015

CA FINAL NOTES ALL SUBJECTS INCLUDING MAY 2015

GROUP I

CLICK HERE TO DOWNLOAD FR NOTES

CLICK HERE TO DOWNLOAD SFM NOTES

CLICK HERE TO DOWNLOAD AUDIT NOTES 2015

CLICK HERE TO DOWNLOAD LAW MODULE 2015

GROUP II

CLICK HERE TO DOWNLOAD COSTING OR NOTES

CLICK HERE TO DOWNLOAD ISCA NOTES 2015

CLICK HERE TO DOWNLOAD DT NOTES 2015

CLICK HERE TO DOWNLOAD IDT NOTES 2015

Subscribe to:

Posts (Atom)